Aside from Visa (V) or Mastercard (MA), it doesn’t seem as if the credit card issuers have been getting the attention they deserve. With all of the panic and concern surrounding the brokers and builders, perhaps plates are too full to take on any more. Yet, I have been thinking about how easy credit policies made available for housing created a monstrous economic problem. Even so, it does seems plausible that companies issuing collateralized debt could eventually see a recovery if the underlying property can be liquidated for some portion of its worth. But, what happens as defaults rise on credit/bank card debt, which is only backed by the full faith and credit of the borrower?

During the past few months, investors have pummeled Discover Financial (DFS) and others lenders over fear of rising defaults and delinquencies. Here is an example of the recent news and behavior of credit companies caused by the subprime problems (2/12/08 Washington Post):

The subprime mortgage meltdown has spilled into the credit card industry in other ways. Banks have reported steep write-offs related to the mortgage mess, and their stock prices have plummeted.

“Credit cards historically have been a very profitable segment for the banking industry, so what they’re doing is trying to squeeze customers as much as they can, particularly for accounts they don’t see as profitable or as high risk,” said Curtis Arnold, founder of CardRatings.com, a consumer resource on credit cards.

Bank of America (BAC), for instance, notified some customers last month that their rates would increase as a result of a periodic review of their credit risk. Chase (JPM) last fall increased the rate paid by new customers of its Freedom card. Bank of America and Chase are also among some banks that have increased ATM fees for other banks’ customers to as much as $3. Capital One (COF) has changed its cash-advance fee for new customers from 19 percent to 23 percent.

Beyond the current economic crisis, there is an even more troubling issue confronting the industry with the pending legislation known as H.R. 5244: (MSNBC Consumerman)

‘The Credit Cardholders‘ Bill of Rights Act of 2008, known as H.R. 5244, would protect cardholders from arbitrary interest rate increases and unfair fees. Maloney, who chairs the House Financial Institutions and Consumer Credit Subcommittee, is quick to point out that her bill does not have any price controls. It does not cap rates or fees.

Interestingly, it looks as though some analysts are continuing to recommend a BUY rating on COF and other names within the sector and are oblivious to the mountain of problems facing bank card companies, aka: The Double Whammy: (Yahoo/AP)

Amid difficulties with mortgages in the U.S. and unloading corporate debt, banks are competing more than ever for market share in their core business — deposits. A large source of profit, banks are introducing newer, higher-yielding accounts to attract more customers’ cash.

The grease that keeps the wheels turning for these companies is capital. In times when money is easily available, bank-card companies utilize their customer accounts to lend money to the credit card customers. As credit card balances rise, new capital is needed to meet the consumer demand.

In order to bring in fresh capital, brokers such as Lehman (LEH), JP Morgan and Goldman Sachs (GS) raise money through note, bond and stock offerings. What do banks do? Of course if they are publicly traded they have the ability to do the same as the brokers and other companies, yet a quieter and quicker maneuver is the bring in new deposits through higher yielding savings accounts. This also helps to bring up the reserve requirements for loans issued through credit card issues and direct loans.

The simple point shows that as customers continue to look for safer alternatives and margins are squeezed as delinquencies and defaults rise, banks that do a big business within the consumer credit card arena could be hit by both problems of limited capital available to loan and ceilings on the fees they can charge for those loans.

The problem for COF is not restricted to our country. Over the past several years, Capital One move aggressively into England and offered attractive terms in order to expand their reach into the credit card business. The New York Times recently explored this problem in the March 22 article entitled, Debt-Gorged British Start to Worry That the Party Is Ending:

…Economists say Britain‘s relationship to debt is complex, but at its core is a phenomenon more akin to recent American history than European trends. As in the United States, a decade-long housing boom and strong economic growth bolstered consumer confidence, creating a perception of wealth almost unknown in countries like Germany and Italy.

…The average British adult has 2.8 credit or debit cards, more than any other country in Europe. A growing number are borrowing to pay for vacations, furniture, even plastic surgery. As a result, Britons are spending more than they earn, racking up a household debt-to-income ratio of 1.62 compared with 1.42 in the United States and 1.09 in Germany.

CNN/Fortune has picked-up on the potential problem back in October, 2007. It is becoming ever apparent that there is a trend that is developing on both sides of the Atlantic. The looming question being asked is; How similar are the problems of British consumers are to those of their Americans counterparts. If England is really an advanced indicator, the pain will be unbearable in the next few months. The $915B bomb in consumers’ wallets:

If there is an international precedent the U.S. should be watching, it’s actually that of the U.K. British consumers are just as overstretched as Americans, but since the real estate market there rose faster and fell earlier, they’re about 18 months ahead in the credit cycle. Since the last quarter of 2005, credit card delinquencies and charge-off rates in Britain have risen as much as 50%, forcing banks to take huge write-offs.

It’s a sign of the times that, according to one survey last month, 6% of British homeowners have been using their credit cards to pay their mortgages. That’s suicidal, of course, given that credit card interest rates are more than double even the heftiest mortgage. Keep your fingers crossed that it’s not a trend that crosses the Atlantic.

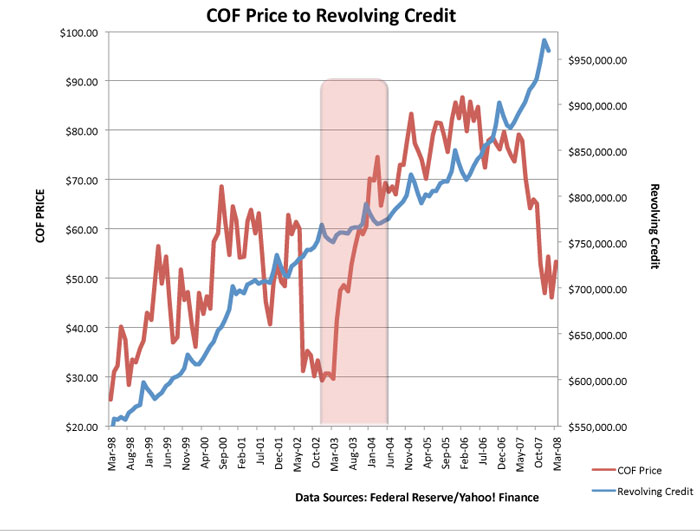

So, that all lead to the main point of the discussion: Capital One Financial. Take a look at business model for the biggest issuer of credit/bank cards in the U.S.:

The National Lending segment consists of three sub-segments: the U.S. Card sub-segment, which consists of domestic consumer credit and debit card activities; the Auto Finance sub-segment, which includes automobile and other motor vehicle financing activities, and the Global Financial Services sub-segment consisting of international lending activities, small business lending, installment loans, home loans, healthcare financing and other diversified activities.

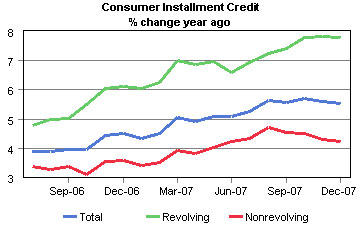

At this stage of our economic cycle, any one of the three sectors would be enough to concern for an investor . This is not the time to be tinkering in an area that has seen a historic contraction without any real plan for recovery. Reports on revolving and non-revolving credit have not been encouraging either. It is perplexing how COF’s stock price has maintained a relatively decent level of support with all of the data and projections available; yet that is exactly why we are zeroing in on this particular company.

The chart above shows the massive increase in revolving credit over the past 18 months. This will only be good for the issuers of credit cards as long as payments stay current. If we see a further increase in late payments and defaults, all bets are off as this stock could nosedive towards the $20 price not seen since 1998. The last time we saw a share price significant slide was during 2002 when the economy was slowing at a rapid pace. The fact is that right now, there are too many headwinds to own this name.

Beyond that, there is one recent piece of news out that needs to be addressed and flushed-out. Odd as it seems, on February 1, 2008, COF’s press release explained of the company’s plan to raise the quarterly dividend from $0.027 to $0.375, payable Feb. 20, 2008 to stockholders of record on Feb. 11. In addition, they put a $2BILLION stock buyback plan into motion. Why? The only thing that can be made of this is an attempt to make it look as though the company is past their problems the management is convinced they will be profitable over the long term. The ugly little truth is that this kind of maneuver allows the company to actually pay less for the dividend, in total, and increases EPS by taking shares off the market. It appears to be nothing more than a move to buy some more time hoping to see if this whole credit crisis will blow over. I am not buying that hype, or the stock!

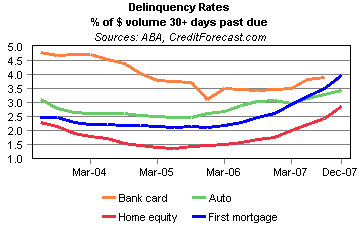

It is abundantly clear that we are seeing a rise in delinquency rates across all credit genres. The only reason that there has been a lag for the bank card component is that consumers have realized that this is the only remaining source of funds as the equity in their homes have dried up and new home equity loans will be difficult or impossible to find. What used to be the order of payments: Mortgage-Auto-Credit Cards has now changed to Credit Cards-Auto-Mortgage. At first this may seem to be a ray of sunshine in an otherwise cloudy forecast. yet, once again, this is actually a more concerning trend as it shows that borrowers are keen to the current need to keep credit available until they exhaust their limits. None of this is very encouraging.

Throughout the country, credit counseling professionals concur. (USA Today 2/28/08)

Credit bureau analyses of consumer payment data show that financially squeezed borrowers have begun paying their credit card and car bills before their mortgages. That’s a striking reversal from the norm, one that reflects rising desperation. It suggests that some people essentially have given up trying to stay current with their mortgages and instead are focused on using credit cards to squeak by.

If the trend persists, many economists say, it could accelerate mortgage losses and further drag down the economy.

Adding further concern is the fact that COF insiders are dumping shares. Whether planned or not, insiders reduced their positions by 10% during the past few months. Keep in mind that this company announced, back in February, a massive buyback program planning to redeem 10% of the total market cap. This points to the obvious strategy of the company’s management to help keep shares artificially high as they are selling. Institutions have also had the same idea and have sold off over 23 million shares during the past 6 months, effectively reducing their positions by 7%.

Needless to say, COF=SHORT for our portfolios. We have been recently begun building a position for clients. There just doesn’t seem to be any good reason to put money into an institution that relies on uncollaterlized consumer debt as its product/inventory. Adding the economic climate, consumer sentiment and the pending legislation does not seem to provide a recipe for success. Sure, anything is possible – but why go long into a position that appears to have so many potential traps?

Econnomic Chart Data Source: economy.com