What could go wrong? That has been the question I have been trying to answer for some time now. The markets have been set up for a bull run and there has been nothing stopping it from going straight north, or is there?

In TDI Podcast 11, (May 27th) we looked at The TOP 10 MISTAKES made when investing. In that show, we explored how this was a key part of the investing process and discussed why they should be avoided at all cost. If nothing else, every once in a while we need to force ourselves to remember these 10 points. It is meant purely as a way to keep us grounded on the road towards successful investing.

Realize that very so often we have a confluence of occurrences that take the market by storm. It may occur in the stock market, but it can just as easily be the real estate markets or perhaps even the commodity markets. In fact, if we look back at the recent run up in the markets, we can see that the global concern over material shortages, coupled with the fact that liquidity entered the markets was a recipe for a swift rise. Add to that the idea that investors needed to find another opportunity after shying away from real estate investments and the stage was set.

Liquidity, did he say liquidity? Yes sir! The forces at play have been amazing. Corporations have been stockpiling cash over the past several years. This was due to profits rising and the cutting of expenses. With so much money sitting in cash (at the beginning of 2007, cash levels of the S&P was at 6.5% total market cap), companies were continuing to buy back their own stock at a blistering pace. Of course this has a significant effect on earnings (see post on buyback problem)

The dollar being weak helps as well. Foreign investment has been rising after all but dried up after 9/11. The increase had been prompted by the belief that investing in the US is safe and the fact that it is cheap. According to the NY Times article by Floyd Norris‘s Off the Charts column on surge in foreign investment of US bonds and stocks; says US Treasury Department reported this week that foreign investors put $68.6 billion in American corporate bonds in May and $42.5 billion in American stocks; notes figures are largest ever for one month; says China, which has huge amounts of dollars to invest, has been growing investor in American corporate bonds, but has not yet shown much appetite for American stocks; holds Japan, which was heavy buyer of American stocks when prices were low in 2002, has become net seller of shares this years.

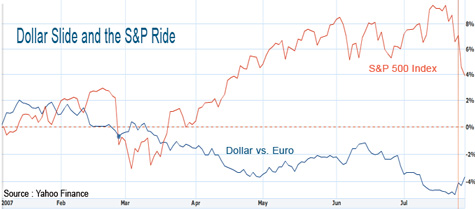

Is it any coincidence that the dollar (versus the Euro as an example) and the S&P 500 are positively correlated these days? Under most circumstances we may be able to put that aside and pay little attention to this. Yet, now is a bit different. I would go so far as to say that the weak dollar has been a significant benefit to the US stocks for tow reasons:

- 1) The weak dollar has increased exports, as foreign money is happy to pay a portion of the usual price for American Goods. This, in turn, benefits earnings.

2) Stock and Bond prices are low as compared to local currency. Why not buy when US stocks are on sale?

This is tempered by the realization that money large companies are considered multi-national and therefore gave currency exposure on a global basis. Non the less, the fact that goods produced and sold in US dollar are cheap as are the stocks of the companies that manufacture them.

With the FED looking like they are moving towards a tightening stance (at least they are not as apt to cut rates) it seems that the slide of the dollar may have finally halted. As the strength of the dollar is very much boosted by a stronger dollar, we may be seeing the end of the record inflow of foreign investment.

This will have a negative effect on liquidity which is already shrinking as private equity is taking breather and lenders are becoming more cautious with their borrowing policies. Add the fact that a slowing real estate market has put a serious crimp on individuals pocketbooks.

If the markets get sapped by any of today‘s villains (sub-prim, terror, Asia sell off, rate hikes, Bill Gross, investor remorse etc) we could see a sell off back to March levels. If my thesis on EPS and Buybacks (link) is even remotely accurate, the domino effect of the above problems will slow corporate buybacks and hurt EPS even more. As investors are focused on growth, the disappointments will lead to additional weakness.

Trees do not grow to the sky and balloons can only stretch so far. Unrestrained optimism (like HUG a Bear comments) needs to be met by a splash of cold water every now and again. The longer we go without a reality check the farther we have to fall. I think 2 steps forward and one step backward is better than 4 steps forward and 3 steps backward any day. Think about that.

Note for the coming weeks: Proceed with caution.